In 1829 Stephenson’s Rocket was cutting-edge but became not-fit-for-purpose due to changing market conditions & requirements, technological innovation and business demands – the world moved-on.

Engineering Construction Business

According to the US Heavy Construction index, as reported by Yahoo! Finance, contractors’ average profits in 2018 were 1.8%. This year, the same index is tracking a $400 million collective industry profit on $94 billion in revenue which is equal to 0.5% profit! What does 2020 hold? The supply chain is not doing much better, if at all.

Those that are doing better than the average should be grateful, but nobody can afford complacency – the contracting business environment is far too fragile. Contrast this with the owners’ experience of uncertain and delayed completion and start-up, substantial cost overruns and challenges in bringing industrial facilities up to and maintaining their full specified operational performance. Whichever way one looks at it the industry does not paint a pretty picture and is not attractive for existing and potential investors.

The Case For Radical Change

While many in the industry are not sitting idly by and hoping for better times to come but are considering and taking measures to improve their lot, the fact is that without radical change the engineering construction industry is not sustainable in the medium term. It is not a matter of tampering with the current models to get slightly better results, because even if these are achieved the ‘success’ will be short-lived. Most of the potential cost and schedule reductions have already been taken out of the traditional-model supply chain.

30-Year-Old-System Not Fit-For-Purpose

The concepts for project delivery and contracting methodologies that have served the industry for the last 30 years or more are no longer fit-for-purpose in today’s world. The notion that obligation and risk can be passed down to the lowest bidders in a supply chain of twelve or more levels and expect effective, efficient and economic performance back up the supply chain is misguided. The amazing thing is that this is nothing new – John Ruskin in mid-19th century England said of doing business “…if you pay too much for something you lose a little money, that is all, but if you pay too little for something then you run the risk of not achieving the thing you wanted…”. How often do owners not get the things that they wanted? … and why is this?

Recent “Successes”

Recent reports of some owner project successes in terms of delivery times and costs may suggest a turning-of-the-corner but when one digs a little deeper into the reported “successful deliveries”, these are not all that they are made out to be. And we must consider that those projects were delivered at a time of low project investment and a high level of resource underutilisation with the result that they attracted a lot of experienced attention. It is not too surprising that they went tolerably well.

Radical Change – What Does It mean?

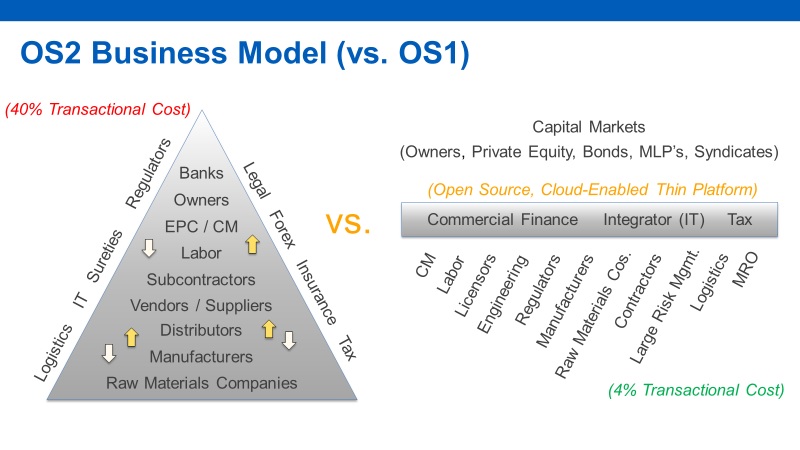

So what does radical change look like? Stephen Mulva (Director, Construction Industry Institute (CII), University of Texas, Austin, TX) illustrates this well in his presentational slide OS2 Business Model (vs. OS1):

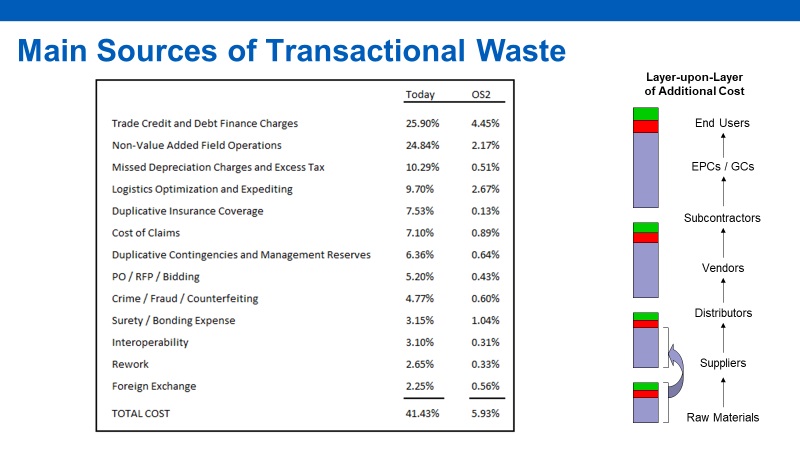

The triangle illustrates ‘OS1’ – ie., Operating System 1 which is the 30-year-old model, and contrasts this with ‘OS2’ which is currently being researched and developed under the auspices of Stephen and the CII. The striking thing is that the inefficiencies of the transactional arrangement in the multi-layered supply chain account for more than 40% of project development costs. The component parts of that 40% are illustrated in another of Stephen’s presentational slides;

It is to be noted that the sum of the figures listed amounts to more than 40%. This is because the CII researchers applied a formula to accurately reflect the overall effect of the individual items listed to arrive at the 41.43%.

But there is another benefit from removing this waste – shortening schedules. This means owners get the products from their new plants to market far quicker.

Tampering With The Old System Will Not Reduce The Costs or Schedule

The fact is that no amount of tampering with OS1 will reduce significantly the transactional costs because they are an intrinsic part of the 30-year-old system. Hence, the system must go and be replaced by something far more efficient – OS2. This will operate on an Open Sourced, Cloud Enabled Thin Platform specifically developed for this industry – currently there is not one. For more information on this follow the link to https://www.constructioninstitute.org.

What Evidence Is There That Such An Approach Works?

Stephenson probably had many nay-sayers when he developed the Rocket – this new-fangled technology will not catch-on – it won’t replace horses! How often has this been said in other contexts – telephone, airplanes, the “wheel”? But Stephenson’s cutting-edge technology in 1829 was soon overtaken by “events” and became not-fit-for-purpose.

Firstly, like it or not, we are living in the age of technology and have been for some while. If like me you are of a certain age, today’s rapidly evolving technology is a challenge! However, the issue is the present and the future, not the past. The industry is already embracing technological advancements cloud-based computing, BIM, digitalisation, artificial intelligence, drones, off-site factory fabrication etc. OS2 utilises these and goes much further.

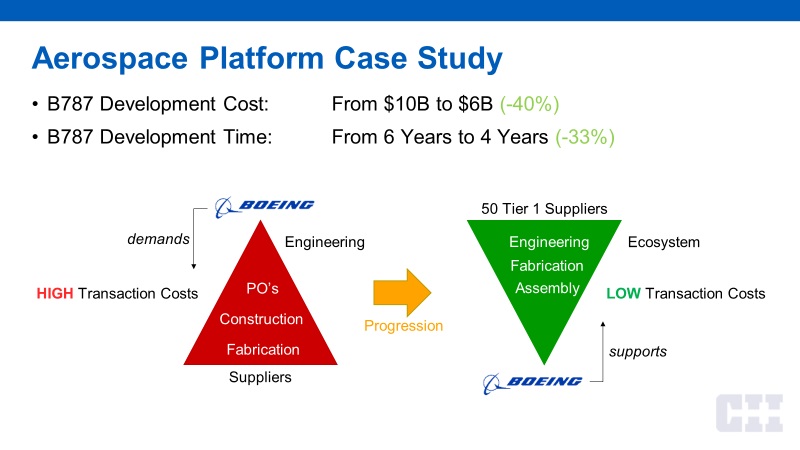

But other industries are far more advanced in this area than engineering construction – shipbuilding, automotive and aerospace are but three examples. Engineering construction is a relative newcomer to technological advancements – why? Again, Stephen Mulva in a presentational slide illustrates Boeing’s approach to the 787 (Dreamliner) development:

It worked – the plane has been operational for some time and is the best thing in the air from an ordinary passenger perspective. Boeing set the tempo that others will have to follow. But think of what Boeing achieved in terms of engineering construction – 40% reduction in development costs and 33% reduction in schedule – and that is fact not myth! I know what will be said – manufacturing in a factory is quite different from construction work on site. Absolutely correct! but isn’t that why the construction industry is turning to maximise off-site factory fabrication and site installation – rather than on-site stick-built construction?

European Construction Institute (ECI)

As ECI Chair I am passionate about fundamental change to improve engineering construction, not just from the commercial business results and sustainability perspective for owners, contractors and the supply chain but also as an attractive career for the next generation of well-educated women and men – it is high time the industry is available to 100% of the population instead of 50%!

The ECI is committed to supporting the CII OS2 initiative. As part of this our focus is on productivity improvement across all construction sectors by working with and learning from organisations engaged in construction sectors in addition to engineering construction. Follow this link to see our approach http://eci-online.org/news/output-from-eci-member-forum-3-april-2019/

What can you contribute to and / or learn from this debate? Why not join in a see what prosperity in engineering construction in the 21st Century might look like. To learn more about ECI and its activities contact us via http://eci-online.org/.

John Fotherby – Chair, European Construction Institute

Chairman, Kingsfield Consulting International